First voice. Then phones. Then cloud. Now AI.

The core problem: The world’s richest people are risking everything on AI: cutting headcount, taking on massive debt, and giving their best people enormous compute budgets, because AI compounds and the gap between first movers and everyone else will become permanent. Elon Musk just offered $60 billion for a 300-person company because the cost of being late to AI is higher than the cost of the bet. So… where’s telco?

Top tech leaders are risking everything on AI. They’re betting their companies, their capital, and their reputations that AI will change everything and that the gap between those who move now and those who move later will soon be too big to close.

- Mark Zuckerberg is spending $125–$145 billion on AI infrastructure this year and cutting 8,000 employees from a company that made $60 billion in profit, because AI can do their work.

- Larry Ellison took on $58 billion in debt, cut up to 30,000 workers, and is running negative free cash flow through 2030 to fund AI data centers.

- Elon Musk had SpaceX acquire xAI, then restructured xAI to improve execution speed (to catch up to OpenAI and Anthropic in AI coding). Two weeks ago, SpaceX secured the right to acquire Cursor, a four-year-old startup with around 300 employees and $2 billion in revenue, for $60 billion.

These aren’t reckless bets. These guys understand that AI compounds, accumulating advantages over time. The more you use it, the smarter your systems get, the faster you move, and the further ahead you pull. And they see that the window to establish that lead is closing.

So, where’s telco?

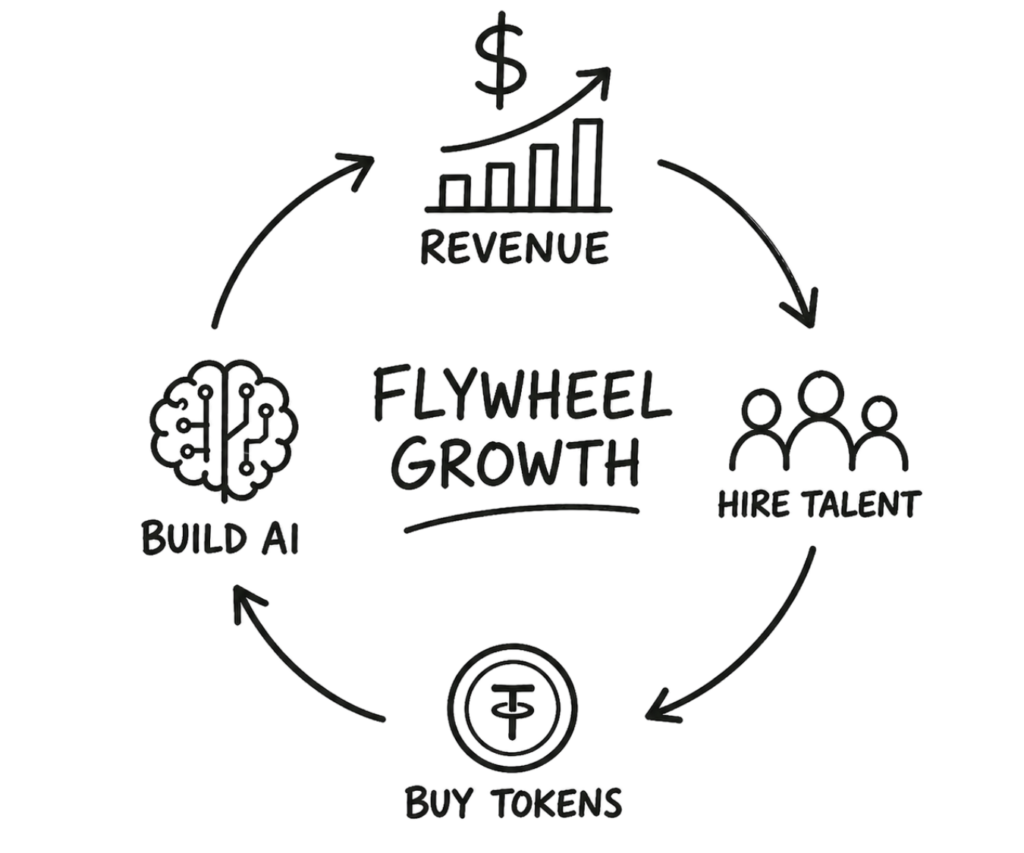

The AI flywheel

AI runs on a flywheel, a self-reinforcing loop where each improvement fuels the next:

That’s what the spending, the layoffs, the debt, and the IPOs are all funding.

Five major US cloud and AI infrastructure providers are expected to spend more than $700 billion on CapEx in 2026, with about 75% of that outlay directed toward AI infrastructure. The intelligence layer—what sits on top of data and workflows to turn information into automated actions—of every industry is getting built right now, and whoever builds it captures the margin.

Is telco investing like this, trying to get first-mover advantages for their own intelligence layer? No. Global telecom CapEx is predicted to fall 2% in 2026 down from the $303 billion spent in 2025. Instead, the industry has its hands in the air wondering who’s going to help us figure AI out. Problem is, the flywheel won’t wait for telco to figure it out. It’s already starting to spin.

Your vendors won’t save you

Telco’s vendors are offering the opposite of compounding. They’re keeping you stuck, and your progress flat. Amdocs just launched an “agentic operating system” while 66% of its revenue came from managed services in 2025. In other words, two-third of its revenue comes from humans operating your systems. Amdocs is selling you AI and headcount on the same invoice.

The tech giants understand something that these vendors don’t. AI doesn’t fractionally improve your existing business. It replaces the architecture of how business gets done. Zuckerberg isn’t cutting 8,000 people because AI makes them 20% more productive. He’s doing it because AI makes them unnecessary.

That willingness to cannibalize your own business model is exactly what’s required at this moment.

You’re being unbundled… again

Benedict Evans warned us about the unbundling phenomenon most recently in his November 2025 presentation, AI Eats the World. Every platform shift (mainframes, PCs, web, smartphones) follows the same pattern: first, incumbents absorb the new technology into existing products. Then startups use it to unbundle the incumbents. That’s how entire industries—and telco—get disrupted.

Telco already lived through this once. WhatsApp didn’t build a better phone network. It built a software layer on top of telco’s infrastructure and took the voice and messaging revenue. Telco built the road. WhatsApp collects the tolls.

It’s happening again. Telco is stuck in phase one of the AI shift, using AI to reconcile overdue invoices and optimize call center scripts. Meanwhile, startups and hyperscalers are already in phase two and three: rebuilding billing systems, building AI-native customer management, and constructing the intelligence layer that will sit on top of telco infrastructure and capture the margin telco keeps leaving on the table.

Every telco CEO says the same thing: we don’t want to be a dumb pipe. We want to be a platform. We want new revenue. And then they issue an RFP, renew the managed services contract, and fund an insignificant tiny AI pilot that doesn’t produce measurable results.

I get the approach: pilots manage the risk of moving. But they don’t manage the risk of standing still. Look around. ARPU is flat. 5G monetization is stalling. The “platform” play remains a slide in a strategy deck. AI is leaping ahead of itself by the month. And while telco waits, the unbundling has already begun.

Break your own rules

You want new revenue? Start buying differently. Start moving differently. Meta didn’t issue an RFP to spend $135 billion. SpaceX didn’t run a year-long diligence process before offering $60 billion for Cursor. They decided and made a bid.

You want to catch up? You’re going to have to break your own rules. Skip the RFP. Break through the analysis paralysis. Kill the pilot that isn’t producing results in weeks. Put AI into production on a real workflow with real subscribers. Measure what happens and make improvements as you learn. Stop waiting for permission.

The richest people on earth are not smarter than telco’s CEOs. They’re not braver. They’re ahead of us because they understand that AI compounds. They did the math and decided that the risk of moving too fast is survivable, but the risk of moving too slow is not. Telco needs to make the same calculation.

The flywheel is spinning. The window is closing. It’s time to make your move.

Recent Posts

Get my FREE insider newsletter, delivered every two weeks, with curated content to help telco execs across the globe move to the public cloud.

Get my FREE insider newsletter, delivered every two weeks, with curated content to help telco execs across the globe move to the public cloud.

Get started

Contact Totogi today to start your cloud and AI journey and achieve up to 80% lower TCO and 20% higher ARPU.

Uncover

What’s blocking telco AI success? The missing piece is a telco ontology that can bridge the gaps between your systems to enable AI at scale.

Engage

Set up a meeting to learn how the Totogi platform can unify and supercharge your legacy systems, kickstarting your AI-first transition.

Understand

Totogi enables the world’s leading operators to move from pilots to operational AI that can reason, decide and act. No rip and replace. Value in weeks.

Our industry is falling behind because we don’t feel the urgency yet. Zuckerberg is spending $125–$145 billion on AI this year and cutting 8,000 jobs at the same time, not because he’s reckless, but because he’s done the math. AI compounds. So, the more you use it, the smarter your systems get, the faster you move, and the further ahead you pull. Telco’s response? Global CapEx fell 2% in 2025. We’re forming committees and issuing RFPs while the rest of the world is building the intelligence layer of every industry. That gap is not going to close on its own.

No. And that’s one of the most dangerous assumptions in the industry right now. Your vendors have a financial incentive to keep you dependent on the architecture you already have. Amdocs just launched an “agentic operating system” for telco while 66% of its revenue comes from managed services, i.e. humans running your systems. It’s literally selling you AI and headcount on the same invoice. Your vendors are not going to help you make them yesterday’s news. You have to take ownership of this shift yourself.

Yes, and it’s already happening. WhatsApp didn’t build a better phone network. It built a software layer on top of telco infrastructure and walked away with the voice and messaging revenue. Telco became the pipe. That unbundling happened because telco moved too slowly. We’re in the same setup right now, just with higher stakes. Startups and hyperscalers are rebuilding billing, customer management, and the entire intelligence layer that will sit on top of telco infrastructure and capture the margin telco keeps leaving on the table. Every telco CEO says they don’t want to be a dumb pipe. But they don’t give themselves any other option when they renew the managed services contracts.

It looks nothing like what most telcos are doing. A real move means putting AI into production on a real workflow with real subscribers and measuring what happens. It means killing the pilot that isn’t producing results instead of renewing it. It means skipping the 12-month RFP process for a decision that needs to happen in weeks. Meta didn’t issue an RFP to spend $145 billion. SpaceX didn’t run a procurement process before offering $60 billion for Cursor. It decided and then moved. Telco’s processes were designed in the past, for a world that moved slowly. That world is gone.

Flip the question. The tech leaders placing the biggest AI bets right now—Zuckerberg, Ellison, Musk—are not smarter or braver than telco’s CEOs. They just looked at the compounding math and made a calculation: the risk of moving too fast is survivable. The risk of moving too slow is not. Telco has been conditioned to see speed as risk. In the AI era, being too slow is the existential threat. The flywheel is already spinning for everyone using AI. The longer you wait, the harder it gets to catch up. At some point, you can’t.